Dubai · United Arab Emirates

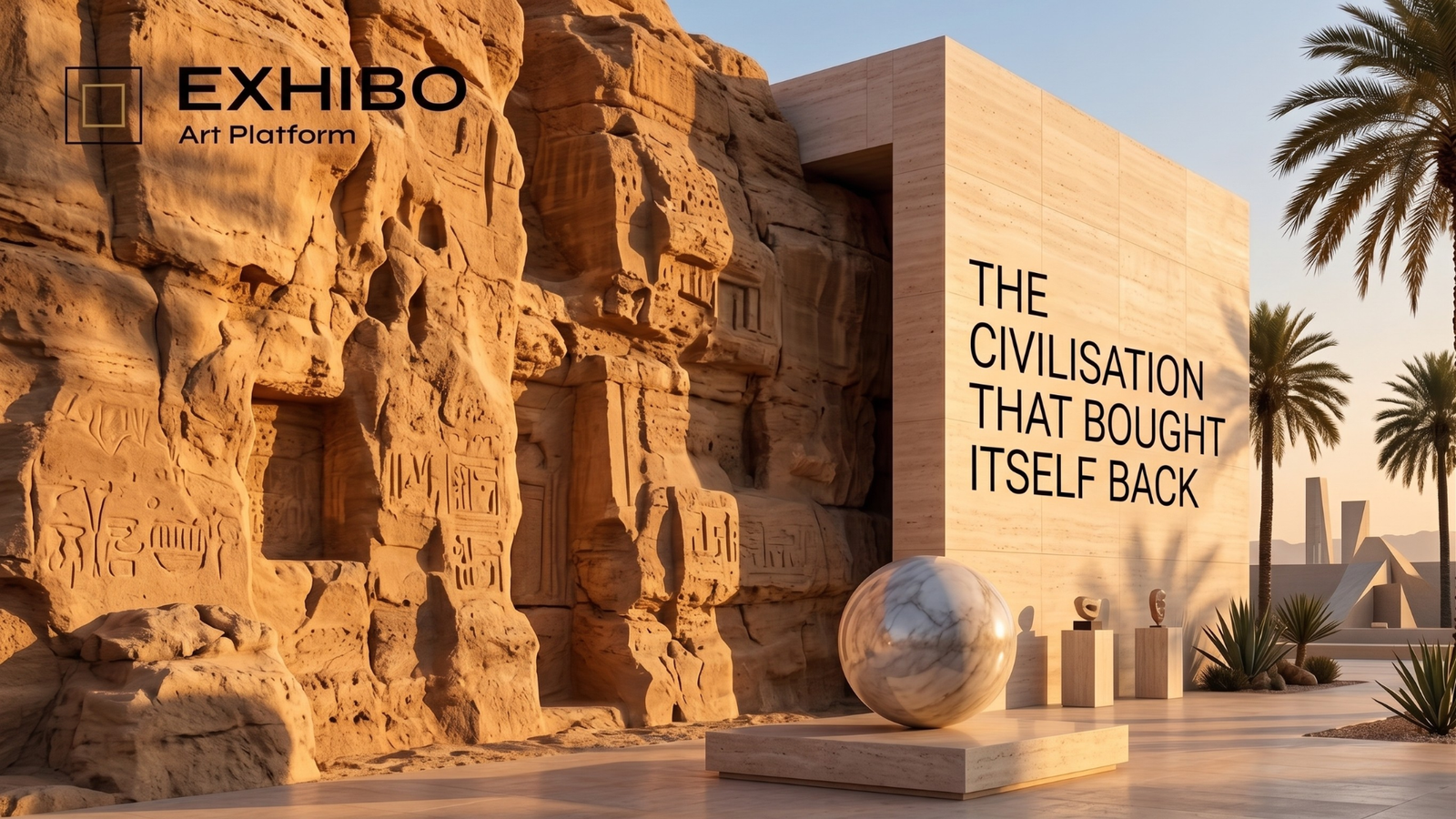

The Civilisation That Bought Itself Back: A Field Guide to Collecting Arab Art

A field guide to collecting Arab and Middle Eastern art — who buys, what it costs, why prices lag cultural significance, and where collectors are looking now.

There are two rooms you have to hold in your head at the same time to understand what collecting Arab art actually means.

The first is in Doha. Sometime around 2011, a painting by Paul Cézanne — The Card Players, one of five versions, the rest in the Met, the Musée d'Orsay, the Courtauld, the Barnes — changed hands in a private sale for a figure widely reported at around $250 million, at the time the highest price ever paid for a work of art. The buyer was the State of Qatar, acting through the woman who has spent two decades as one of the most influential figures in the global art world: Sheikha Al Mayassa bint Hamad bin Khalifa Al Thani. Her annual acquisitions budget has been estimated by Bloomberg and The New York Times at around $1 billion. A Cézanne. A Rothko at $72.8 million. A Gauguin reportedly near $300 million. This is collecting as nation-building — the deliberate creation of cultural capital, at a scale and ambition the art world had not seen since the great state collections of an earlier age.

The second room is a living room in Beirut. Starting in the early 1970s, a Lebanese businessman named Ramzi Dalloul and his wife Saeda began buying art — not Cézannes, but the work of Arab painters and sculptors most of the world had never heard of, picked up during his business trips across the region. He bought because he believed in pan-Arabism, because he wanted to archive the political and social reality of the Arab world through the eyes of the people he considered its most reliable witnesses: its artists. Over fifty-five years the collection grew to more than 4,000 works. He never built the museum he dreamed of. He died in 2021, and his son turned the holdings into a foundation.

Same verb — to collect — two completely different undertakings. One is a sovereign wealth fund pointed at Western masterpieces to build cultural capital in a single generation. The other is a private act of memory, conducted quietly over half a century, to keep a regional history from disappearing. And these are only two of at least four distinct logics by which the Arab world has set about acquiring art — its own and everyone else's — over the past hundred years.

The headlines only ever cover the most expensive one. This is a field guide to all of them: the hundred-year head start the West got, the state-as-Medici machine of the Gulf, the believers who saw value before the market did, and the moment — happening right now — when the market finally caught up. By the end you should understand not just who buys Arab art and why, but the argument this guide will build toward: that the gap between how culturally significant this art is and how much it costs is, by the standards of any comparable canon, unusually wide — and closing. That is a thesis, not a theorem; you cannot prove it the way you prove a sum. But it is one the chairman of Christie's Middle East has himself put on the record, in almost those words, and it is the single most useful idea for anyone thinking about this field as a collector.

Part I. The Hundred-Year Head Start

To understand why collecting Arab art feels, in 2026, like a frontier — like something being discovered rather than continued — you have to understand a strange historical inversion. For most of the twentieth century, the most important collections of art from the Arab and Islamic world were not in the Arab world. They were in London, Paris, New York and Geneva.

The clearest monument to this is the Khalili Collections. Nasser David Khalili, a London-based scholar-collector of Iranian origin, assembled what is widely regarded as the finest private holding of Islamic art on earth: more than 28,000 objects spanning some 1,400 years — Qur'ans, illustrated manuscripts, ceramics, glass, metalwork, scientific instruments, arms and armour, carpets. The catalogue alone was conceived as a 47-volume scholarly series under the general editorship of Julian Raby, the former director of the Smithsonian's Freer Gallery. The collection's own scholars rank it among the best in the world; when a selection went on show at the Emirates Palace in Abu Dhabi in 2008, it was, at the time, among the largest exhibitions of Islamic art ever staged.

Sit with the geography of that for a moment. An Iranian-born collector in London accumulates the material heritage of the Islamic world, and then exhibits it back to the Gulf, to Paris (the Institut du Monde Arabe), to Amsterdam, to Sydney. The art travelled west during the long century when wealth, museums and the apparatus of connoisseurship lived in the West; now it travels back east as the wealth does. This is not a morality tale of theft and restitution — much of this material was collected, catalogued and preserved by Western scholars and institutions with real care, and that scholarship is part of why it survives at all. It is something more interesting than a grievance: a shift in the centre of gravity of who studies, stewards and values this art. That shift is the deep structure beneath everything else in this story.

The market for classical Islamic art still runs on this Western-built infrastructure, and it sets records that dwarf almost anything in the modern category. A folio from the Shahnameh of Shah Tahmasp sold for £8.1 million in 2022, the highest price ever for an Islamic work on paper. An early Islamic bronze figure of a buck — Umayyad, eighth-century — made £4.2 million in October 2024, a record for early Islamic sculpture. A blue-and-white Iznik pottery charger reached £5.4 million in 2018 (all per Sotheby's Islamic Art department). This is a deep, mature, scholarly market — and it is almost entirely separate from the market for modern and contemporary Arab art that the rest of this guide is about. A collector entering one is not automatically a collector in the other. They have different specialists, different auction calendars, different price logics, and largely different buyers.

The capitals that made the art — and then lost it

Here is the painful part. While the collections of Islamic art were being built in the West, the production of modern Arab art was happening in a handful of cities that the global art world barely looked at: Cairo and Alexandria, Beirut, Baghdad and Damascus. As Sotheby's specialist Ashkan Baghestani has put it, "the cultural capitals of the Arab world were once Beirut, Damascus, Baghdad and Cairo" — long before the Gulf, with its hydrocarbon wealth, started building creative infrastructure from scratch.

Cairo and Alexandria gave the movement its founding father. Mahmoud Said (1897–1964) — the son of a prime minister, trained partly in Europe, a judge who abandoned the bench at fifty to paint full-time — produced the canonical images of Egyptian modernism: the women of Alexandria, the Nile at dusk, the dervishes mid-spin. There is a museum dedicated to him in Alexandria. His Whirling Dervishes (1929) sold at Christie's in 2010 for $2.54 million; his late Vue de la plage à Cassata en Grèce (1964) became the most expensive work by an Arab artist sold at auction in 2024, passing $1 million against an estimate of $470,000. Around him orbited a remarkable generation: Abdel Hadi El-Gazzar, the surrealist whose Fishing set a record of $746,500 in 2011 at a Christie's sale that itself blew past expectations to total $8 million; Inji Efflatoun, simultaneously a Marxist activist, a feminist and — for six years — a political prisoner.

Baghdad produced what may be the most intellectually ambitious chapter of the entire story. In 1951, the sculptor Jewad Selim and the painter Shakir Hassan Al Said founded the Baghdad Modern Art Group and issued a manifesto — the first art manifesto published in Iraq, an event many scholars treat as the birth of Iraqi modernism. Their idea, istilham al-turath ("seeking inspiration from heritage"), refused the choice between imitating the West and retreating into nostalgia: they reworked Sumerian sculpture, Abbasid manuscript painting and the thirteenth-century Baghdad school of Yahya al-Wasiti into a genuinely contemporary language. Selim is best known for the Nasb al-Hurriyah (Freedom Monument) on Baghdad's Tahrir Square, a fifty-metre bronze relief he died before completing. Al Said, who outlived him by four decades, drove the idea further into pure abstraction, founding the "One Dimension" group in 1971 and developing — under the influence of Sufism and the mystic al-Hallaj — the practice of turning the Arabic letter into an abstract, contemplative sign. This is hurufiyya, "letterism," the calligraphic abstraction that stretched from Baghdad to Cairo to Beirut and that now functions, for better and worse, as the most recognisably "Arab" gesture on the market.

And then Baghdad gave the story its tragedy. The Iraqi national collection of modern art was largely looted or destroyed in the chaos following 2003. So much was lost that documentation — letters, catalogues, photographs — now stands in for the missing objects in exhibitions of the period. The works that survived did so mostly because they had already left: the great Iraqi modernist holdings that come to market now — the Madhloom, Makiya, Jawdat and Parker collections — were almost all assembled by people who carried them out of Iraq in the 1960s and 1970s. This is the origin of one of the most important practical truths for anyone collecting in this field: in a region where art has been destroyed, displaced and dispersed, provenance is not paperwork. It is the asset. A work with an unbroken, documented history of ownership is worth more — sometimes dramatically more — than an identical work without one, because the unbroken history is itself rare. On the Bonhams Baghdadiyat sales, Selim's Women Waiting made £125,250 and Al Said's Hob al-Watan min al-Iman £175,250 — prices underwritten as much by their pedigree as by their paint.

Beirut was the cosmopolitan hub. Before the civil war (1975–1990), the Sursock Museum and its annual Salon d'Automne, the American University of Beirut, and a dense circuit of galleries nurtured Saloua Raouda Choucair (the pioneering abstract sculptor who studied alongside Léger in Paris and now sits in MoMA, the Met, Tate and the Pompidou), Paul Guiragossian (born in Jerusalem to survivors of the Armenian genocide), Shafic Abboud, Etel Adnan, Aref El Rayess, Helen Khal. Their biographies read as flight itineraries — Beirut, Paris, Alexandria, Venice, São Paulo — by the early 1960s. The market is now reappraising this "Beirut generation" aggressively: Lebanese modernist Huguette Caland set a personal record at $565,000 in 2023; a work by Etel Adnan made £252,000 against a £30–40,000 estimate.

The point of this history is not nostalgia. It is causation. The reason collecting Arab art feels like a discovery is that the canon was assembled with half the evidence missing — the production happened in cities that lost their museums, their archives and sometimes their objects, while the connoisseurship lived elsewhere. Everything happening now in the Gulf is, in one way or another, an attempt to close that hundred-year gap.

Part II. The State as Medici

The first and loudest answer to that gap is money — public money, deployed at a scale and speed without precedent in the history of art. But "the Gulf is buying art" is far too crude a statement to be useful. There are two distinct state models, and the difference between them is the difference between two philosophies of how you manufacture culture.

Doha: grow your own

Qatar's strategy, under Sheikha Al Mayassa, has been to grow institutions organically rather than import them — to reject the franchise model that its neighbours embraced. The flagship is Mathaf: Arab Museum of Modern Art, which opened in 2010 with a collection now exceeding 9,000 works — the largest dedicated holding of modern and contemporary Arab art anywhere in the world. Around it sit I. M. Pei's Museum of Islamic Art (2008) and Jean Nouvel's National Museum of Qatar (2019), with Herzog & de Meuron's Lusail Museum (around 2029) and the Art Mill Museum (around 2030) still to come.

What makes Mathaf significant for collectors is not the building but the genealogy of the collection. Its core came from one man: Sheikh Hassan bin Mohammed Al Thani, who from the early 1990s built a private holding of more than 6,000 works — including what is considered the largest collection of Iraqi art in the world, assembled in part by supporting Iraqi artists after the Gulf War. In other words, the single most important museum of Arab modernism was seeded by a private collector with conviction, decades before the state formalised it. That pattern — private passion converted into public canon — recurs throughout this story.

The scale of Qatari buying is striking, even allowing for the fact that the state rarely confirms figures. As early as July 2011, The Art Newspaper identified Qatar as the world's biggest buyer in the art market by value, behind most of the major modern and contemporary deals of the preceding years. Market analysts of the period noted the country's willingness to pay above prevailing prices to secure the works it wanted. The lesson for a collector is not the specific number but the structural point behind it: when a committed buyer of that scale enters a category, it tends to lift the whole field with it — which is exactly why what the Gulf's state collections pursue is worth watching closely.

Abu Dhabi: import the brand

Abu Dhabi took the opposite road: license the world's most trusted cultural names and plant them on a single island. The Saadiyat Cultural District has been costed at $27 billion, one of the largest cultural investments of its kind in the world. Its anchor, the Louvre Abu Dhabi, opened in 2017 under a 2007 intergovernmental agreement that licenses the Louvre name until 2047 — a deal the Louvre itself has described as France's largest cultural project abroad. Crucially, the museum is not just a borrowed brand: it has built its own permanent collection, beginning with nineteen acquisitions unveiled in 2009 (including a fourteenth-century Mamluk Qur'an and a Mondrian) and continuing with everything from Roman cameos to Kandinsky and Giacometti.

The long-delayed, Frank Gehry-designed Guggenheim Abu Dhabi — set to be the largest Guggenheim in the world — has been quietly building a collection of modern and contemporary art from West Asia, North Africa and South Asia since 2009. In December 2025, two more mega-museums opened on the island: the Zayed National Museum and a Natural History Museum (per The Art Newspaper). In 2021 the emirate committed a further $6 billion to creative industries on top of the billions already spent.

For a collector, the practical implication of the two state models is this: institutional money is writing the canon of Arab art in real time, and it is doing so with deep pockets and long horizons. When Mathaf or the Guggenheim acquires an artist, it confers a durable institutional credential — the kind of recognition that, historically, the market has tended to price in over time. Watching what the state museums collect is, on that reading, one of the more reliable leading indicators available: these are buyers who do not need to sell, and whose validation has often preceded price appreciation by years.

Culture as national vision

What is easy to miss from the outside is how deliberately this has been designed, and how closely it tracks each state's own stated priorities. These are not vanity projects; they are explicit instruments of national development. The UAE frames culture as a pillar of its post-oil, knowledge-economy future. Saudi Arabia's Vision 2030 sets a measurable goal — culture and the creative industries reaching around 3% of GDP — and treats the arts as central to economic diversification, youth employment and national identity. Qatar's museum programme, in Sheikha Al Mayassa's own framing, is about "globalising the local and localising the global" — building institutions that tell the region's story on its own terms rather than importing someone else's.

The scholarly literature reads this, rightly, as a sophisticated exercise of cultural diplomacy. As one academic survey of the Gulf puts it, the success of these states' soft power lies in their ability to attract, finance and own some of the world's most respected cultural institutions — and to do so while building genuine local capacity: curators, conservators, art historians, audiences. The institutions are also developing thoughtful, locally grounded curatorial frameworks; the forthcoming Lusail Museum, Al Mayassa has said, is intended to "spark conversations about decolonisation, multiple representation, tolerance and peace." This is a region defining what a museum can be in its own cultural and legal context, not simply replicating a Western template.

For a collector, the practical takeaway is that this is a state-led, vision-driven market in its institution-building phase — backed by long-term public commitment and patient capital. That is a source of unusual stability: few art markets in history have enjoyed this depth of committed, long-horizon support. It also means the pace and emphasis of the build-out are shaped by national strategy, which a serious collector does well to follow closely, because it signals where recognition — and value — are heading next.

Part III. The Believers

If the state model is the loudest, the most instructive — for an actual collector — is the quietest: the private collectors who bought Arab art out of conviction, decades before there was a market to validate them. They are the ones whose example actually translates into a strategy.

The pan-Arabist: Ramzi and Basel Dalloul

Return to that Beirut living room. Ramzi Dalloul's collection — more than 4,000 works built over fifty-five years — was an ideological project before it was ever a financial one. His son Basel formalised it into the Dalloul Art Foundation (DAF) in 2017, continued acquiring at a pace of forty-plus works a year, and entered the ARTnews Top 200 collectors. The ideology is captured perfectly in an anecdote told by a fellow collector: Dalloul once asked him not to bid on a Gibran Kahlil Gibran work at auction, so that it could stay in Lebanon — "I can't only show an Egyptian intellectual here in Lebanon without also showing a Lebanese intellectual."

The Dalloul story also illustrates something every collector should internalise about how value is created in this market. When Christie's sold forty-eight works from the collection in its 2023 Marhala sale, they made around $3 million. Christie's specialist Hala Khayat described the logic behind such collections in a line that ought to be printed on the wall of anyone starting out: "A lot of the works we are selling now from collectors are the fruits of friendship. Someone believed in the artist back in the 1950s when no one was looking at his work. It takes a long time — you have to be passionate, and not look for the monetary value." The fruits of friendship. The value was created by conviction held over decades, not by timing the market.

The counter-argument: Sultan Sooud Al Qassemi

The other essential private figure is Sultan Sooud Al Qassemi, the Emirati writer and Columbia professor who began collecting in 2002 and founded the Barjeel Art Foundation in Sharjah in 2010. Barjeel now holds well over a thousand works of modern and contemporary Arab art (recent counts put it past 1,800), and since 2018 has shown a long-term selection at the Sharjah Art Museum. Its travelling exhibition Taking Shape: Abstraction from the Arab World, 1950s–1980s toured American university museums between 2020 and 2022, and a dedicated Barjeel museum is under construction in Sharjah.

What makes Barjeel different from the state model is its explicit purpose. Al Qassemi has described the collection not as an asset but as a counter-argument — to the idea that the history of modern art was made in New York and Paris and that everywhere else was peripheral. Sharjah, in this sense, plays a role in the regional ecosystem that the commercial hubs cannot: it is the non-commercial, curatorial, intellectual counterweight, the place where the canon is argued rather than priced. For a collector, Barjeel functions as the single best free education in the field — its collection, much of it viewable, is a map of who matters and why.

The Saudi pioneers

Saudi Arabia, by contrast, has institutional ambition that is, for now, well ahead of its still-young private collector base — the number of established Saudi collectors remains relatively small, and those who have led the way tend to act as champions for the wider scene. Basma Al Sulaiman, who started collecting in the 1990s (her first purchase a Hockney), has turned her holding of Saudi art into a memorial to her late son. Hamza Serafi, co-founder of Jeddah's Athr Gallery, collects Saudi artists from the 1960s to the present — Abdulhalim Radwi, Ahmed Mater, Nasser Al Salem, Dana Awartani. The structural gap is stark, and one statistic captures it better than any other: Saudi private wealth exceeds $2.4 trillion, yet buyers from the Kingdom account for just 0.01% of those million-dollar-plus art purchases, and family offices there allocate around 1% to art against a global average of 7%. As one local figure put it, "the money is not moving because nobody has packaged the opportunity properly." That sentence — and the institutional build-out racing ahead of the private market it describes — is worth returning to, and we will, because Saudi Arabia has become central to where this market goes next.

The lesson the believers teach is the most actionable in this entire guide, and it is almost embarrassingly simple: the people who made money in Arab art are the ones who bought it before it was a market, because they actually looked at the work. Conviction precedes price. It always has.

Part IV. The Market Catches Up

For most of the period covered above, the believers were alone. Now they are not. Beginning around 2005–2006, the commercial apparatus of a real art market arrived in the Gulf — and over the past five years it has gone from curiosity to one of the most dynamic segments in the world. This is the part of the story most relevant to a collector deciding whether and how to enter now.

How Dubai became a market

The conventional story credits governments. The truer story starts with a marble factory. In 2007, an Emirati businessman named Abdelmonem Bin Eisa Alserkal owned a cluster of warehouses in Al Quoz, an unglamorous industrial district nobody in the art world had thought to look at, and offered subsidised space to galleries willing to commit to a permanent, year-round presence. Ayyam Gallery moved in first in 2008, with a programme built on Syrian and broader Arab contemporary art. Others followed. By 2015, Alserkal Avenue had grown to 500,000 square feet; today it houses more than a hundred galleries, studios and cultural organisations and draws over two million visitors a year. The same year Alserkal made his bet, Art Dubai launched its first edition. Two private wagers, one year, the same proposition: that Dubai could be a serious art city, not a luxury-tourism backdrop with gallery-adjacent hotel lobbies.

What grew on that foundation is a genuine ecosystem. In Dubai, galleries such as The Third Line (one of the first UAE galleries accepted into Art Basel), Lawrie Shabibi, Green Art Gallery, Grey Noise, Isabelle van den Eynde and Tabari Artspace (operating since 2003) built international reputations. The DIFC Gate Village clusters Christie's, Sotheby's, Perrotin and a dozen others within walking distance. In Saudi Arabia, Athr (Jeddah, since 2009) and Hafez anchor a fast-emerging scene; in Beirut, Agial / Saleh Barakat and Galerie Tanit sustain one of the most intellectually serious gallery cultures in the world through repeated crisis. The auction houses followed and then doubled down: Christie's has run dedicated Dubai sales since 2006; Sotheby's, which had been working out of Doha and Dubai, opened its first permanent Saudi office in Riyadh in 2025 and is opening permanent space in Dubai.

The numbers — and the paradox at the centre of them

Here is the single most important fact for understanding this market, and it cuts against everything the breathless coverage implies. Since 2011, total public auction sales of fine art by Middle Eastern artists have surpassed $399 million — and that figure represents less than 1% of the global fine-art auction market by value. A tiny sliver. The entire category is, in dollar terms, a rounding error against the Picassos and Basquiats of the global market.

Now hold that next to its opposite. Middle Eastern collectors accounted for 23% of global demand for contemporary works priced above $1 million in the past year (a figure attributed to the art-investment platform Qantara). Christie's reports that 15% of its new global clients over the past three years came from the Middle East and Africa. Abu Dhabi's sovereign wealth fund ADQ took a minority stake in Sotheby's itself.

Read those two facts together and you have the defining paradox of the field: the art is a sub-1% niche; the buyers are a global force. The region produces a fraction of the world's auction turnover but a disproportionate share of its serious demand. That asymmetry is not a weakness. For a collector, it is the single most striking feature of the landscape — a market where the appetite, the wealth and the infrastructure have arrived years ahead of the prices for the region's own art.

And the prices are moving. The momentum, by the numbers:

- Christie's reports that sales of modern Middle Eastern art in the UAE trebled in value between 2020 and 2024 (per market analysis).

- A ten-year study shows MENA auctions grew 30–40% between 2013 and 2023.

- Contemporary Middle Eastern art sales in London rose 89% year-on-year in Q1 2025; New York consignments jumped 67%.

- The global auction market itself rebounded hard into 2026: combined sales at Christie's, Sotheby's and Phillips rose 64% to $1.7 billion in Q1 2026, the strongest first quarter since 2016, on stronger demand at the top end (ArtTactic, via The Art Newspaper).

- Sotheby's 2023 dedicated sale totalled $6.1 million, its highest since the category's 2016 relaunch, with more than ten works above $300,000.

- Sotheby's 2025 MENA sales drew collectors from 23 countries, a third of them new to the house; its debut Riyadh Origins sales achieved a combined $10 million and set five world records.

- Online art sales across the Middle East and Africa reached $1.41 billion in 2024, with mid-single-digit annual growth forecast to 2033 (Grand View Research, via Zurani).

- The UAE alone has committed close to $5.3 billion to arts and cultural infrastructure; art-linked tourism across the region generated over $3 billion in 2024.

The most useful confirmation, though, comes not from a number but from the people setting the prices. After Christie's November 2025 London sale — where a Saloua Raouda Choucair sculpture more than tripled its high estimate — Ridha Moumni, the house's chairman for the Middle East and Africa, described what is happening as MENA artists "seeing a rapid correction in their individual markets after decades-long undervaluation." When the chairman of Christie's MEA uses the word undervaluation on the record, the central premise of this guide stops being an outsider's thesis and becomes the house view.

And the record book that this momentum is rewriting reads like a roll call of the artists from Part I finally being priced:

| Artist | Origin | Record (auction) | Note |

|---|---|---|---|

| Parviz Tanavoli | Iran | ≈ $2.5m (2008) | The Wall (Oh Persepolis) — long the region's auction record |

| Mahmoud Said | Egypt | $2.54m (2010); >$1m (2024) | the founding father of Egyptian modernism |

| Fahrelnissa Zeid | Jordan/Turkey | up to ≈ £2.7m | among the most expensive women artists of the region |

| Farhad Moshiri | Iran | > $1m (2008) | the first Iranian contemporary to break seven figures |

| Safeya Binzagr | Saudi Arabia | $2.1m (2026) | a landmark for the Saudi market, at Sotheby's Riyadh |

| Mohammed Al Saleem | Saudi Arabia | $1.1m | among the highest for a Saudi artist; pioneer of "Horizonism" |

| Abdel Hadi El-Gazzar | Egypt | $746,500 (2011) | the Egyptian surrealist's record |

| Huguette Caland | Lebanon | $565,000 (2023) | record for the artist |

| Saloua Raouda Choucair | Lebanon | £393,700 / ≈$500,000 (2025) | Poem (1966–68), more than tripling its high estimate |

| Samia Halaby | Palestine | $485,000 (2023) | Seventh Cross No 229 |

| Shakir Hassan Al Said | Iraq | £175,250 | Hob al-Watan min al-Iman, Bonhams Baghdadiyat |

(Figures are hammer or hammer-plus-premium as reported by the auction houses, Artprice and Artnet; currency conversions are approximate and record years may be superseded.)

The economics of a fixed supply

There is one more force under all of this, and it is the part of the argument the breathless coverage almost always misses, because it is about supply rather than demand. The masters at the centre of the modern canon are gone. Mahmoud Said died in 1964. Jewad Selim died in 1961, the Freedom Monument unfinished. Shakir Hassan Al Said died in 2004. Saloua Raouda Choucair, Paul Guiragossian, Etel Adnan — the generation that made Arab modernism is, almost to a person, no longer producing. The body of work is closed. Every painting that will ever exist by these artists already exists, and a meaningful share of it was lost, in Iraq especially, to war. The supply is not just finite; it is, for the canonical names, fixed and in some cases shrinking.

Now set the demand against it. Mathaf and the Guggenheim Abu Dhabi are, in the words of The Art Newspaper, ramping up acquisitions after years-long lulls; Saudi Arabia's Ministry of Culture is buying at pace to fill the institutions rising across Diriyah; Barjeel and the private foundations keep collecting; and a new generation of regional buyers is entering every season. Fixed supply, rising institutional and private demand — that is the whole of the economic case, stated in a sentence, and it is the most durable reason the believers' bet has tended to pay off.

What is releasing that fixed supply onto the market right now is a generational handover that deserves to be understood as a market event in its own right. The great private collections of Arab modernism were assembled, for the most part, by a single founding generation in the 1960s and 1970s — and that generation is now passing its holdings to heirs and foundations. The Bonhams Baghdadiyat sales drew their Iraqi masterpieces directly from the Madhloom and Makiya family collections; the Dalloul holdings passed from Ramzi to his son Basel; estates connected to figures like Neziha Selim, sister of Jewad, have begun to surface at auction. This is why so much exceptional material has appeared in the last few years: not because the art was suddenly made, but because a first generation of collectors is handing it on. For a buyer, this is the rare and probably temporary window in which canonical works circulate before they settle, very likely for good, into the permanent collections of the region's new museums.

And this finally explains the word undervaluation properly — because the undervaluation was never a verdict on the art. It was a verdict on the infrastructure around it. For most of the twentieth century the work was, as one senior Lebanese collector put it, hidden by conflict and war: people simply did not know the artists. There were no international dealers championing them, no English-language narrative placing them in the global story, no world-class museums in the region to anchor their value, and only the thinnest thread of integration into the Western canon. Wars scattered the archives; absent estates made provenance hard to establish. None of that was about the quality of a Said or a Selim. It was about everything around the painting — and almost every one of those gaps is now, at last, being closed. That is the real content of the "correction" the auction houses describe: not the art changing, but the world finally being built around it.

Why the structure favours the buyer

Beyond momentum, the UAE offers structural advantages that are real and specific, not marketing: zero personal income tax, zero capital gains tax on art, and a free-trade-zone infrastructure enabling bonded storage and efficient cross-border transacting. The houses themselves describe Gulf buyers not as opportunistic flippers but as collectors building with long-term intent and holding power — and the friction costs that erode returns in New York or London are simply lower here.

But the most telling structural fact is the gap itself. A Mahmoud Said making $1 million is extraordinary by the standard of where this market was a decade ago — and modest by the standard of what a comparable European figurative painter of the same period commands. The institutional recognition (Mathaf, Tate retrospectives, the Pompidou, MoMA acquisitions) has largely arrived; the market price, in many cases, has not fully followed. Works by Arab modernists whose museum credentials are established but whose prices still lag remain available, in many cases, in the $20,000–$80,000 range. Whether that gap narrows is not guaranteed — no market gap ever is — but it is the thing a serious collector will want to understand before anything else, because it is where cultural significance and price are currently furthest apart.

Where this argument could be wrong

Honesty requires putting the other side of that case as plainly as the case itself, because the gap between recognition and price is not a law of nature. Museum recognition does not reliably convert into sustained price appreciation. Institutional support is not the same thing as market liquidity. A wave of cultural-infrastructure spending does not guarantee that the works themselves will rise in value, or stay risen. The history of art is full of cautionary precedent: there are major Latin American and African modernists with deep critical reputations and museum holdings whose markets stayed relatively shallow for decades, and some still have. Recognition can outrun demand for a very long time — sometimes a working lifetime, sometimes longer. The thin secondary market discussed earlier cuts both ways: it can mean prices have room to rise, but it also means there may be few buyers on the day you want to sell. Everything in this guide describes conditions that have historically favoured patient collectors in this kind of moment. None of it is a promise about the next decade. The honest version of the thesis is not "Arab art will appreciate." It is: "the distance between how this art is regarded and how it is priced is unusually wide, the reasons for that distance are closing, and that is an interesting place for a collector who looks carefully to be — with eyes open to the risk that the market may take far longer to agree than the museums already have."

A word on the calligraphy trap

One caution that separates informed buyers from tourists. The single most recognisable gesture on this market is calligraphic abstraction — hurufiyya — and it is simultaneously the field's deepest intellectual tradition (Al Said, El-Salahi, Madiha Umar) and its most over-supplied cliché. Specialists note that buyers reflexively reach for "a calligraphic element", and that a market saturated with one safe gesture — like the glut of "women in veils" that specialists warn about — devalues. Worth knowing, too: much of what a Western eye reads as Arabic "calligraphy" in Iranian work (Moshiri, Mohammed Ehsai) is in fact lettrism — the play of letters drained of meaning, "about the beauty of the thing." Buying the gesture because it looks reassuringly "Arab" is how people overpay. Buying the artist because the work is rigorous is how the believers in Part III made their returns.

The living market: contemporary, and the Saudi engine

Everything so far has leaned on the modern masters, because that is where the canon and the clearest pricing gap sit. But the modernists are, by definition, a closed set — and for most new collectors the actual point of entry is not a 1960s Baghdad canvas but a living artist whose work can still be bought from a gallery at an approachable price. The contemporary layer is where the scene is most alive, and it is worth knowing by name. Hassan Sharif (1951–2016) is now regarded as the father of conceptual art in the Gulf. Around and after him: Mohammed Kazem and his GPS-mapped coordinates; the Emirati conceptualists of the "Five"; Kuwait's Monira Al Qadiri, whose iridescent oil-industry sculptures have entered major collections; the Egyptian Wael Shawky, who designed the inaugural Art Basel Qatar and whose film-based work runs through the Venice Biennale; the Palestinian Dana Awartani, working in geometry, tilework and repair. These are artists with international gallery representation, biennale histories and museum shows — and prices that, for now, frequently start in the four and low five figures.

Nowhere is the contemporary turn more consequential than in Saudi Arabia, which is no longer a footnote to this story but, increasingly, its centre of gravity for future growth. A decade ago the Saudi scene was an artist-led, almost underground affair — the touring exhibition Edge of Arabia, founded in 2008 by Ahmed Mater, Abdulnasser Gharem and Stephen Stapleton, carried Saudi art around the world before the institutions existed. What has happened since, under Vision 2030, is one of the fastest state-led cultural build-outs anywhere on earth. The Ministry of Culture, founded in 2018, now sits above a dense and growing apparatus: the Diriyah Biennale Foundation, which launched the country's first contemporary art biennale in 2021 and whose third edition opened in January 2026 with more than 65 artists from over 37 countries; the alternating Islamic Arts Biennale in Jeddah; the Misk Art Institute in Riyadh, whose founding director was Ahmed Mater; Noor Riyadh, the world's largest light-art festival; Desert X AlUla; 21,39 Jeddah Arts; and Hayy Jameel, Art Jameel's Jeddah complex. The physical heart of much of this is the JAX District in Diriyah — a regenerated estate of more than a hundred former warehouses that the Ministry of Culture has designated as the country's reference arts district, now home to studios, galleries and the Biennale itself, with a Saudi contemporary art museum and a Centre Pompidou partnership among the institutions still to come.

A constellation of Saudi artists has risen with this infrastructure: Ahmed Mater, whose work documenting the transformation of Mecca made him the first Saudi to hold a solo show in the United States; Manal AlDowayan; Abdulnasser Gharem; Maha Malluh; Muhannad Shono. For a collector, the significance is twofold. First, this is where the demand of the next decade is being manufactured — the institutions filling these new museums are buyers, and the audiences they are building are tomorrow's collectors. Second, the Saudi case captures the central paradox of this whole guide in miniature: the wealth is vast, the state is building cultural infrastructure at a pace the world has not seen before, and yet the private collecting market is only just beginning — recall that buyers from the Kingdom still account for a fraction of a percent of global million-dollar art purchases. The supply of serious work is here; the institutions are here; the wealth is here. The connective layer that turns all of that into a functioning market is the part still being built.

Part V. The Honest Mechanics of a Young Market

A guide that sold only the upside would be a brochure, not a field guide. The features below are not flaws so much as the natural characteristics of a market still in its building phase — and a collector who understands them is far better placed than one who does not.

Depth is still developing. Liquidity for many regional artists is still building, and the secondary market remains younger than the fast-growing primary one. Outside the established names, reselling can take patience. This is, in the best sense, a market to enter with conviction and a long horizon — which, as Part III showed, is exactly how its most successful collectors have always approached it.

It is anchored by long-term public commitment. A large share of the investment that built this ecosystem comes from government and institutional sources pursuing multi-decade national visions rather than quarterly returns. That patient, strategic backing is a genuine strength — it has produced world-class infrastructure at a speed no purely commercial market could match. It also means the build-out follows national priorities, so reading those priorities (Vision 2030, the UAE's cultural strategy, Qatar's museum roadmap) is part of reading the market. The encouraging trend is that organic, private demand is now growing alongside the public foundation — the two are beginning to reinforce each other.

The region has shown real resilience. The wider environment can be eventful. In 2026, regional circumstances briefly affected logistics: Art Dubai's twentieth-anniversary edition shifted from April to May and ran at a more intimate scale. The Iranian market — historically one of the largest forces in MENA auctions, accounting at points for a substantial share of the category's value — has developed its own resourceful ecosystem, including a strong turn toward digital and time-based work (a dynamic studied in detail in the academic literature).

And here is the reassuring part. That more intimate 2026 Art Dubai still drew over 25,000 visitors — a record for public attendance — with Taymour Grahne selling out a solo booth of Emirati artist Roudhah Al Marzouei in the opening hours. The collector base that showed up was overwhelmingly local and regional: not flown in, not dependent on outside validation, simply people for whom this is their own scene and their own market. That is what a market built on real foundations does when conditions get complicated. It holds.

The honest summary is this: these are the characteristics of a young, fast-maturing market, and they make the case for entering with knowledge, not for staying away. The same asymmetries that give a casual buyer pause are exactly what leave room for the informed one.

Part VI. The Map Doesn't Exist Yet

Step back, and the shape of the whole thing resolves.

For a hundred years, two mechanisms decided what counted as significant art. Museums recognised it slowly, through acquisitions and retrospectives, on timescales measured in decades. Then auction prices accelerated the process, turning money into a proxy for significance. But both mechanisms share the same blind spot, and it is worth stating as plainly as possible: museums and auctions are mechanisms for recognising what has already been recognised. Neither is built to find the unfamiliar. Both confirm; neither discovers. That single limitation explains why Arab modernism could sit in plain sight for fifty years while the canon was written without it — and why a Choucair sculpture could be admired by Le Corbusier and acquired by MoMA and still leave its maker effectively unknown until a Tate retrospective in her ninety-eighth year. The art was never missing. The mechanism for noticing it was.

What changed is that a different infrastructure got built — by the believers, the foundations, the warehouse landlords, the gallerists who committed when there was nothing to validate them, and, decisively, by the national cultural visions of the Gulf states that turned individual conviction into lasting public institutions. Mathaf and Barjeel and the Dalloul collection. The Louvre Abu Dhabi and the coming Guggenheim. Alserkal Avenue and Athr and Ayyam. The auction departments and the biennials. Diriyah and Saadiyat and the Doha museum mile. They created, between them — private passion and public vision reinforcing each other — the structure for a different kind of looking: one capable of recognising significance before the museum and the auction record confirm it. It is one of the great cultural-infrastructure achievements of the century, built in a single generation.

That structure is now mostly in place. What is still missing is the layer that connects it to the people who would engage with it if they could find their way in — the collector in Singapore who read about Arab modernism in the Financial Times, the buyer in London weighing their first regional purchase, the curator in São Paulo who heard The Third Line mentioned on a panel. The art is real. The galleries are real. The prices are still, for now, on the favourable side of a gap that may or may not stay open. The one thing that does not yet exist is the map: a way to see how a scene fits together, what its galleries mean, where its artists sit, and why any of it matters — before you need a personal introduction or a plane ticket to find out. That gap, between supply that exists and demand that cannot find it, is the last piece of infrastructure this market is waiting on.

The believers were right about one thing above all, and it is the note to end on. The work was always there. The only question, in every decade of this story, was whether anyone was looking. What is happening now is larger than a market cycle and larger than any single collection: it is a civilisation rebuilding the infrastructure of its own cultural memory after a century on the periphery — assembling the museums, the scholarship, the canon and the public that a culture needs in order to know, and value, itself. The art market is only the most visible edge of that project. More people are looking now than at any point in a century. The map of it all does not exist yet.

That is the opportunity — for collectors, for institutions, and for anyone who understands that the next chapter of art history is being written, right now, in a region the rest of the world spent a hundred years overlooking.

About Exhibo

*Exhibo is a discovery platform for emerging art markets, beginning in the Gulf and expanding across MENA. It helps collectors, galleries, journalists and institutions navigate local art scenes — mapping galleries, artists and exhibitions by city and district, with the context that makes a scene legible to someone who isn't already an insider. If the gap this article describes — between art that exists and the people who would value it if they could find it — is one you recognise, that is the gap Exhibo is built to close.

Galleries mentioned

Museums mentioned

Related reading

Editorial

EditorialSomewhere Between a Marble Factory and a Masterpiece

On the art world's transparency problem, the extraordinary markets the world is only beginning to discover, and why we decided to build a map.

February 2026, Doha. Msheireb Downtown — the old business district that Qatar has been quietly transforming into something between a cultural quarter and an ur…

Editorial

EditorialWorld Art Dubai 2026: Dates, Curators and What to Expect at Expo City

The fair's 12th edition moves to a new venue, introduces a dedicated photography section and expands its mentorship programme — here is everything you need to know.

World Art Dubai returns for its 12th edition from 19 to 22 November 2026, this time at a new home — Dubai Exhibition Centre at Expo City. With over 10,000 works from 65 countries, a new dedicated photography section and an expanded mentorship programme, here is everything galleries and collectors need to know.

Editorial

EditorialArab Modernism 101: The Movement That Western Art History Forgot

An entire century of extraordinary painting, sculpture and radical thinking got written out of the global canon. Someone made that decision. And now the market — and the collectors who pay attention — are making a different one.

Great art does not become invisible by accident. Arab Modernism reveals how museums, markets and cultural institutions shape what the world sees — and what it overlooks. A story about artists, recognition and the blind spots that define art history.